Mine Ledger: $HCC (Warrior Met Coal - 6/9/2024)

- thecommoditiesboy

- Jun 9, 2024

- 4 min read

(Disclaimer: Literally none of this is financial advice. If you take this as financial advice, the only thing you better be sending me are sad cat gifs. I am not liable for your financial gains or losses - this is just my uninformed opinion. Also everyone should be properly credited for their work - if I didn't let me know and I'll fix it)

Current Performance Snapshot (As of Close 6/7/2024):

__________________________________________________________________

Price as of June 7, 2024: $67.59

Market Cap: $3.54B

P/E Ratio: 8.13

Dividend Yield: 0.47%

__________________________________________________________________

Daily Chart Snapshot:

__________________________________________________________________

Macro Fundamentals:

To me, $HCC is a play on two things - the APAC region with the Chinese and Indian economies resurgent and the fact that coal is not dead. Specifically metallurgical coal (and thermal too but that's a story for another time).

Everyone keeps harping on the the green revolution and meeting IPCC goals of whatever the *C target we've set (and that we're going to miss). Whatever that case might be, it's undeniable that the green revolution is going to be powered by steel.

Every solar farm, every wind mill, everything green energy needs steel. And you know what you need to make steel? Coal - more specifically metallurgical coal.

And g*dd*mn, but China and India have been buying up coal and making record amounts of HRC (Hot Rolled Coil) steel.

Let's take a gander at the Chinese outlook according to a screengrab I pulled from S&P Global:

What we're seeing here is that despite the industrial and real estate slowdown in China, as their economy comes back to life (as the CCP drags it kicking and screaming), they're making more and more steel and exporting more and more.

And we're seeing this feeding into their surging coal demand. A quick gander at their import/export website (http://english.customs.gov.cn/Statics/4778123c-8cfa-4253-b2e7-0e8c808021e0.html) shows us that their coal imports are surging over 12.6% year over year (highlighted in green):

Of course, a good chunk of this does flow in from Australia (so think $YAL or $WHC) but as they saw, a rising tide does lift all boats.

A similar quick look at the India side shows a similar story (in writing this piece I learned that the Ministry of Coal is a thing in India).

Total coal imports are up a whopping 13.9% from Y21/22 to Y22/23. With a stated target of doubling total steel production capacity from Y22 numbers by 2030, I'm only salivating thinking about where it can go next.

Lastly, while Australia does make up the bulk of the exports, the US is rapidly increasing their export capacity. As pulled from the EIA Quarterly Coal Report:

A whopping annualized 10.4% increase in met coal exports with Asia alone increasing by 34.7%

The absolute kicker, look at how much our exports to China increased - an eye-watering 95.6%...

Anyway, I'll let you ruminate on that for a bit...

__________________________________________________________________$HCC Fundamentals:

HCC is a beauty. The strongest met coal margins out of all major producers by a country mile.

Currently, they produce around 8 million tons of met coal per year out of their two mines in Alabama with access to around 25 years of reserves (so around 200 million tons)

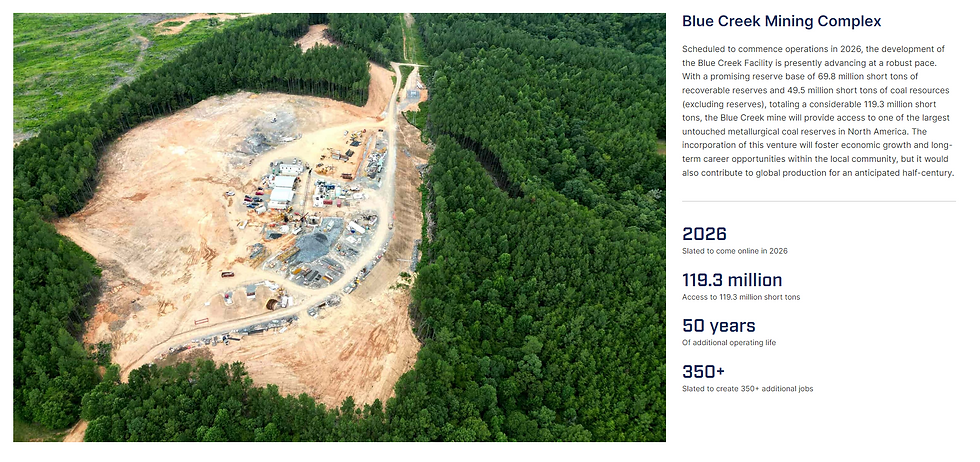

With their Blue Creek mine coming online this is what we're looking at:

50 years of operational life with 119.3 million short tons. Let's break that down with some papernapkin math:

119.3/50 = 2.386 million short tons (assuming that's what they maintain in annual production).

Just off of that, they're increasing production by a whopping 30%. Now imagine they continue those current margins.

The beauty of all of this is that they are self financing. So whatever drag we see in their net income is all derived from their own cash flow.

So yes, a simple google search will tell you the outlook isn't so good.

But guess what, all of this is Blue Creek. Once Blue Creek starts producing, we're looking at a papernapkin math surge in revenue by around 30% - so around $650M+ in revenue. A massive decrease in cost will follow pumping up the net income.

But you probably want numbers, so let's look into it from their own earnings:

A good chunk of their costs are simply from Blue Creek valued between $335-$390M (let's take $335M). Let's say once that 2026 rolls around, we're taking that off the table. In the worst case, we add $100M in cap exp for existing mines. So let's make that $210M.

The net change: $235M added back into the equation for income/profit. So we're suddenly looking at net income of at least $372M (give or take).

Guess where that takes the EPS?

Assuming that the outstanding shares stay somewhere around current levels (52,163,000)

7.1...

That's more than double. Of course, you got other expenses or whatever it might be (who knows), so let's knock it down to 6eps

That's still more than doubling your EPS...and you can let that feed into your share price.

I'll see you at $120+ on HCC :)

(The kicker is that HCC still beat ER estimates)

Risks to Consider:

Chinese economy downturn (again)

Blue Creek financing issues and/or operational issues

__________________________________________________________________

ComBoy Outlook:

Bullish

The Original Hawk Tuah Video Girl – Hilarious Memes

YouTube Adblocker: Block YouTube Ads in 2025

Save YouTube™ Thumbnail – Chrome Extension

The Connection Between Scrum Pillars and Team Happiness

Watch One Girl One Wolf One Frog @@ Viral Video

Funny Memes – Best Memes of The Week

NyanCat – Memes, Drawing, Song, Game and NFT

MonsNode Alternatives in 2025: Top 6 Platforms

Streameast Alternatives: Legal Sites to Stream Sports Live

Kelly Bates Asks Supporters NOT to Take Out Their Anger on NBC 10

HCOOCH CH2 H2O: The Hydrolysis of Methyl Formate

Dubai Metro Map (PDF) – Your Guide to Routes and Stations

Techbullion Logo & Company Profile

Mysterious Tale of Selena Green Vargas, Where Did She Go?

trwho.com: Your…